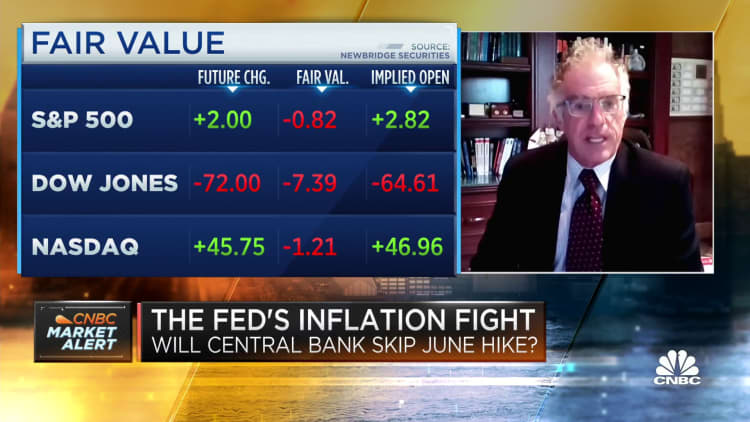

Traders are signaling that a pause in interest rate hikes is the most likely outcome of this week’s Federal Open Market Committee meeting of the Federal Reserve, and that comes at a time when some strategists are saying a new bull market is underway. The Dow Jones Industrial Average posted three winning sessions in a row to end last week, the NASDAQ Composite saw its sixth-consecutive positive week for the first time since November 2019, and all major indices closed above their 50-day and 200-day moving averages on Friday.

“The bear market is officially over,” Bank of America equity strategist Savita Subramanian recently said, noting that the S&P 500 has risen 20% above its October 2022 low.

Some question the new bull market call based on how narrow market leadership has been — a handful of the largest tech stocks responsible for much of the rebound in market indexes. But there is another important reason investors should not become overconfident. Even if the Federal Reserve decides to pause when it announces its latest FOMC decision on Wednesday, a longer-lasting shift by the Fed in its most aggressive period of monetary policy since the 1980s is by no means certain, or warranted.

That’s according to former Federal Reserve vice chair Roger Ferguson.

Last month, the Fed approved the tenth interest rate hike in just over a year, the swiftest monetary policy tightening that the central bank has undertaken since the 1980s, with significant repercussions not only for the stock and bond markets, but for the economy and consumers. In its May FOMC meeting statement, the Fed removed language about the need for “additional policy firming” in order to achieve inflation goals. That’s helped sustain the majority view in the market that a pause will be announced this week.

But Ferguson remains unconvinced.

“I think the pause here is really a closer call than the market currently expects,” he said in an interview with CNBC’s “Squawk Box” on Friday. And even if the Fed does pause, Ferguson says it doesn’t mean that more rate hikes aren’t coming over the rest of the year.

“The market should brace itself for a Fed that is going to continue to be hiking even if this one happens to be a pause,” Ferguson said.

He isn’t alone in the view that a Fed pause won’t last long. “We think the Fed ends up skipping this month, but setting the table for actions in July,” said Michelle Girard, head of U.S. at NatWest Markets, in an interview with CNBC’s senior economics reporter Steve Liesman last week.

A pause is highly likely, according to former Atlanta Fed President Dennis Lockhart. However, he noted in an interview with CNBC’s “Closing Bell Overtime” that inflation will continue to pose an issue for the Fed. “There are some signs that can be grasped of declining inflation, but it is very gradual. I think the committee still has a big challenge, particularly with a 2% target,” Lockhart said, referring to the Fed’s stated goal of bringing inflation back down to a target range of 2% over the longer term.

On an annual basis, the inflation rate was 4.9% in April, slightly less than the market estimate, but it remains “sticky,” both as observed in prices throughout the economy, and in the expectations of many CEOs on the record as saying inflation will persist. This upcoming week will include the latest read on the annual and monthly inflation trend with the May consumer price index report due on Tuesday, the first day of the Fed’s two-day FOMC meeting.

Traders react as Federal Reserve Chair Jerome Powell is seen delivering remarks on a screen, on the floor of the New York Stock Exchange (NYSE), May 3, 2023.

Brendan McDermid | Reuters

Ongoing concern about inflation is one of the factors that leads Ferguson to see a higher possibility of a hike come Tuesday. This view is underpinned by, among other things, a labor market that continues to be tight. Wage growth has cooled, and unemployment is rising. But Ferguson cited the approximately 1.7-1.8 jobs for every unemployed person, far higher than the norm; and wages that have continued to go up, not only in the recent national data but also in terms of what he is hearing anecdotally from CEOs — Ferguson is on the board of directors for multiple large corporations, including Alphabet and Corning.

“I think overall the picture is one of inflation and inflation pressures that are higher and stickier than the 2% number that the Fed has been aiming for. So I think it’s the data that’s already here that’s telling us more hikes on the way,” he said.

Others see recent cooling the labor market as a signal the Fed may soon have more need to moderate its rate hike strategy. Wharton professor Jeremy Siegel recently told CNBC that while the Fed has expressed strong commitment to lowering inflation, the central bank’s dual mandate is achieving its target inflation rate and promoting maximum employment. On a historical basis, unemployment remains extremely low — under 4% —but jobless claims recently hit the highest level since October 2021.

“I’m talking about trend here,” Siegel said.

For now, the Fed can be “as aggressive and hawkish as they are,” Siegel said, because there has not been much of a pickup in unemployment, and workers continue to feel confident about their job market prospects. There are some signs that worker confidence is on the decline. The latest consumer confidence index reading from the Conference Board showed that consumer assessment of current employment conditions experienced “the most significant deterioration” in May among consumer sentiment data it tracks. Labor economists have told CNBC that on balance the latest data from the labor market supports Fed Chair Jerome Powell’s view that the central bank can engineer a soft landing for the economy.

“There is nothing here that makes me think we are not in a soft-landing scenario,” said Rucha Vankudre, senior economist at labor market consultant Lightcast in a recent interview after the May nonfarm payrolls report. “I wouldn’t be surprised if the Fed decides to keep rates where they are. All indicators are the economy is going in the right direction.”

Nick Bunker, director of economic research at Indeed Hiring Lab, says all the recent data points are broadly in line with the soft-landing hypothesis. “The broad picture here is the labor market is cooling in a sustainable way. There are signs of moderation and not a ton of red flags,” Bunker said.

But there is an old saying on Wall Street that the job market is always the last to know when a recession hits.

“Let me say one thing,” Siegel told CNBC. “If we get a negative job report within the next month, next two months, it’s going to hit headlines, first time since Covid. And then people are going to say, ‘Oh, can I be assured that I’m going to get another job?’ And that’s going to play into politics and I think is going to pressure the Fed on the other side, and then they’re going to begin to say, ‘Okay, maybe inflation is going to get better.”

Goldman Sachs recently lowered its house view on the odds that the U.S. economy enters a recession, but its own CEO David Solomon — who remains convinced higher inflation will be persistent — and Ferguson, remain unsure about how future Fed decisions will shape the economic outlook. Solomon said at the recent CNBC CEO Council Summit that “some structural things going on” related to inflation will make it hard to “easily” get back to the Fed’s 2% target, and even if the Fed pauses, based on what he sees now in the economy there is no expectation of rate cuts by the end of the year — an outcome bond traders have been betting on.

Ferguson fears that high levels of inflation may force the Fed to increase rates to a level that effectively force the U.S. into a recession. “I am still in the camp that recession is a real possibility. Short and shallow one hopes, but you know, let’s see, and let’s hope Goldman is right,” Ferguson said.

Former Fed Governor Frederic Mishkin shares concerns about inflation, and believes the proper Fed course is to not pause in June.

“I can understand why [the Fed] might want to [pause], it’s not terrible if they do it,” Mishkin said in a recent CNBC interview. “But I think that we’re in a situation where inflation numbers are still high, very slow to come down towards the 2% target.”

Mishkin is more worried, he said, about the underlying inflation, which is a number that is reliable in predicting what the future path of inflation will be. “The economy and labor market is still strong, there is some weakening but we’ve got a long way to go before we contain inflationary pressures and therefore I think that the Fed is going to have to raise rates, and better off doing it now to show their strong commitment to keeping inflation under control,” he said.

A pause would be unlikely to pose significant harm to the economy, even if subsequent rate hikes are needed, Ferguson said, pointing to examples of “early pausers” — the Bank of Canada and Reserve Bank of Australia. “Both took a pause and now have returned to a hiking process,” he said.

Stay connected with us on social media platform for instant update click here to join our Twitter, & Facebook

We are now on Telegram. Click here to join our channel (@TechiUpdate) and stay updated with the latest Technology headlines.

For all the latest World News Click Here